How Vega Affects Long Calls and Long Puts

You've been there. You buy a call option on a stock that you're absolutely certain is about to rip higher. The stock moves in your favor. You check your P&L expecting fireworks, and instead you see a modest gain. Or worse—a loss. Seriously. The stock went up, your call went down. How is that even possible?

The culprit is almost always Vega. And if you've been trading options for any length of time, you know this isn't some obscure Greek from a finance textbook. It's the invisible hand that slaps you around when implied volatility shifts. Honest? It's one of the most misunderstood levers in options trading, especially for long-dated positions. Let's dig into how Vega specifically impacts both long calls and long puts—and why ignoring it can cost you real money.

---

The Hidden Variable That Moves Your P&L

Most new traders fixate on Delta. Stock goes up, call goes up. Simple, right? But options aren't simple—they're four-dimensional beasts. Vega measures an option's sensitivity to a 1% change in implied volatility. It's not about how much the stock moves; it's about how much the market expects the stock to move.

Here's the thing: every option price bakes in a volatility assumption. When you buy a call or a put, you're not just betting on direction. You're betting on whether the actual volatility (realized vol) will outpace what's already priced in (implied vol). Vega is your exposure to that gap.

I can't tell you how many times I've watched traders pile into long calls ahead of earnings, only to get crushed the next day even though the stock moved exactly how they predicted. That's the Vega hangover. You're long vol going into an event, and the moment the uncertainty disappears, implied volatility collapses. Your call bleeds value from the Vega drop faster than it gains from the direction.

It's a big deal.

Why Vega Hits Harder on Longer-Dated Options

Look—Vega is not uniform across all expiration cycles. It scales with time to expiration. A 60-day option has significantly higher Vega than a 7-day option on the same underlying. The market is pricing in more potential volatility over a longer horizon, so any shift in that expectation hits the premium harder.

- Long-dated calls and puts have higher Vegas. A 1% IV move on a 90-day option can swing your position by several hundred dollars per contract. - Short-dated options have low Vegas. IV can jump 5% and you might barely notice the change in your P&L.

This creates a sneaky problem for long-term bull or bear trades. You buy a long call six months out because you love the stock. Two weeks later, the market calms down, IV contracts, and suddenly your call is worth 20% less even though the stock hasn't moved a cent. You're now underwater on a position that hasn't yet had time to prove itself. That's the Vega tax on directionally-neutral time.

---

How Vega Specifically Shapes Long Calls

Let's get into the mechanics. A long call gives you positive exposure to both Delta (stock up) and Vega (vol up). In theory, that's a beautiful combination. In practice, it's a double-edged sword.

When implied volatility rises—say, during a market panic or ahead of a catalyst—your long call gains value purely from that volatility expansion. The stock doesn't even need to move. I've seen calls gain 30% on days where the underlying barely budged, all because fear spiked. That's the Vega tailwind.

But volatility has a nasty habit of reverting to the mean. When conditions stabilize, implied volatility contracts. Your long call loses value from that contraction. And guess what? Theta is also working against you every single day. So you've got two Greeks pulling your position down (Theta and negative Vega during IV contraction) and only one Greek pushing it up (Delta, if the stock moves your way).

Here are a few practical ways Vega hits your long call:

- Post-earnings IV crush: You buy a call before earnings. IV is inflated. The company reports a great quarter, stock gaps up 5%, yet your call barely gains because IV drops 10 points. - Market regime shifts: During a 'risk-off' event, VIX spikes, your calls look great. A week later, the Fed calms everyone down, VIX plummets, and your calls lose value despite stock staying flat. - Time decay acceleration in high vol environments: High IV means higher extrinsic value. When IV collapses, that extrinsic value evaporates. Your long call premium gets hit from both sides.

Seriously, if you're buying long calls without monitoring implied volatility levels, you're gambling blindfolded. Track the IV rank. Know whether you're buying into historically high vol or low vol. It changes everything.

The Asymmetric Vega Exposure on Long Puts

Long puts operate under the same Vega mechanics, but the context is wildly different. Puts are hedges. They're insurance. And insurance gets expensive when fear is high.

Here's a counterintuitive truth: long puts can actually benefit from Vega more aggressively than calls in certain environments. Why? Because volatility tends to spike during market selloffs. When stocks crash, fear explodes, and implied volatility for puts (especially out-of-the-money puts) can go parabolic.

If you're holding a long put during a crash, you get a double whammy in your favor: the stock falls (positive Delta) and implied volatility skyrockets (positive Vega). Your put gains value from both directions simultaneously. It's glorious. It's also rare.

But here's the nasty flip side. Buy a long put during a calm market as a hedge against a crash that doesn't happen. Vol remains low. The stock grinds higher. Your put loses money from Delta, Vega, and Theta. Triple threat.

- IV expansion during crashes: Massive wins for long puts. Vega adds a premium on top of directional movement. - IV contraction after fear subsides: Even if the stock stays low, your put loses value as the market calms down. - Holding through vol mean reversion: If you buy puts when IV is already elevated, you're fighting Vega from day one. The market will eventually calm, and your put will decay faster than expected.

I had a client once who bought long puts on a major index during a brief volatility spike. The index hadn't really crashed—it just shook a bit. He was convinced the world was ending. Two weeks later, IV normalized, the index recovered slightly, and his puts were worth pennies. The stock never even dropped 5%. Vega slaughtered him.

---

Managing Vega Risk in Directional Trades

So what do you actually do about this? You can't ignore Vega. You have to manage it. Here are the tactics I use and teach after a decade of watching traders get wrecked.

Pick your entry points wisely. Don't buy long calls or long puts when implied volatility is at the 90th percentile of its 52-week range. You're buying overpriced options. Wait for IV to contract. Buy when the market is calm and options are cheap. You sacrifice some potential upside if the stock moves immediately, but you significantly reduce your Vega risk.

Use vertical spreads to offset Vega exposure. A long call vertical (buy a lower strike, sell a higher strike) reduces your Vega exposure because the short call offsets some of the volatility risk. You trade away unlimited upside for a defined risk profile with less sensitivity to IV changes. Same goes for puts. It's not sexy, but it works.

Pay attention to IV skew. Not all options on the same stock react the same to volatility. Puts often have higher implied vol than calls (skew). If you're buying a long put, you're buying the expensive side of the skew. Factor that into your thesis.

Here's a quick list of what to check before entering any long call or long put:

- What is the current IV rank? (Above 70%? Be careful.) - Is there an upcoming catalyst (earnings, Fed meeting, data release)? - How much Vega does each contract have? (Your broker's platform shows this. Use it.) - What is the VIX doing? Is it trending up or down? - Can you stomach a 10% drop in option value from IV contraction alone?

If you can't answer these, you're not ready to trade.

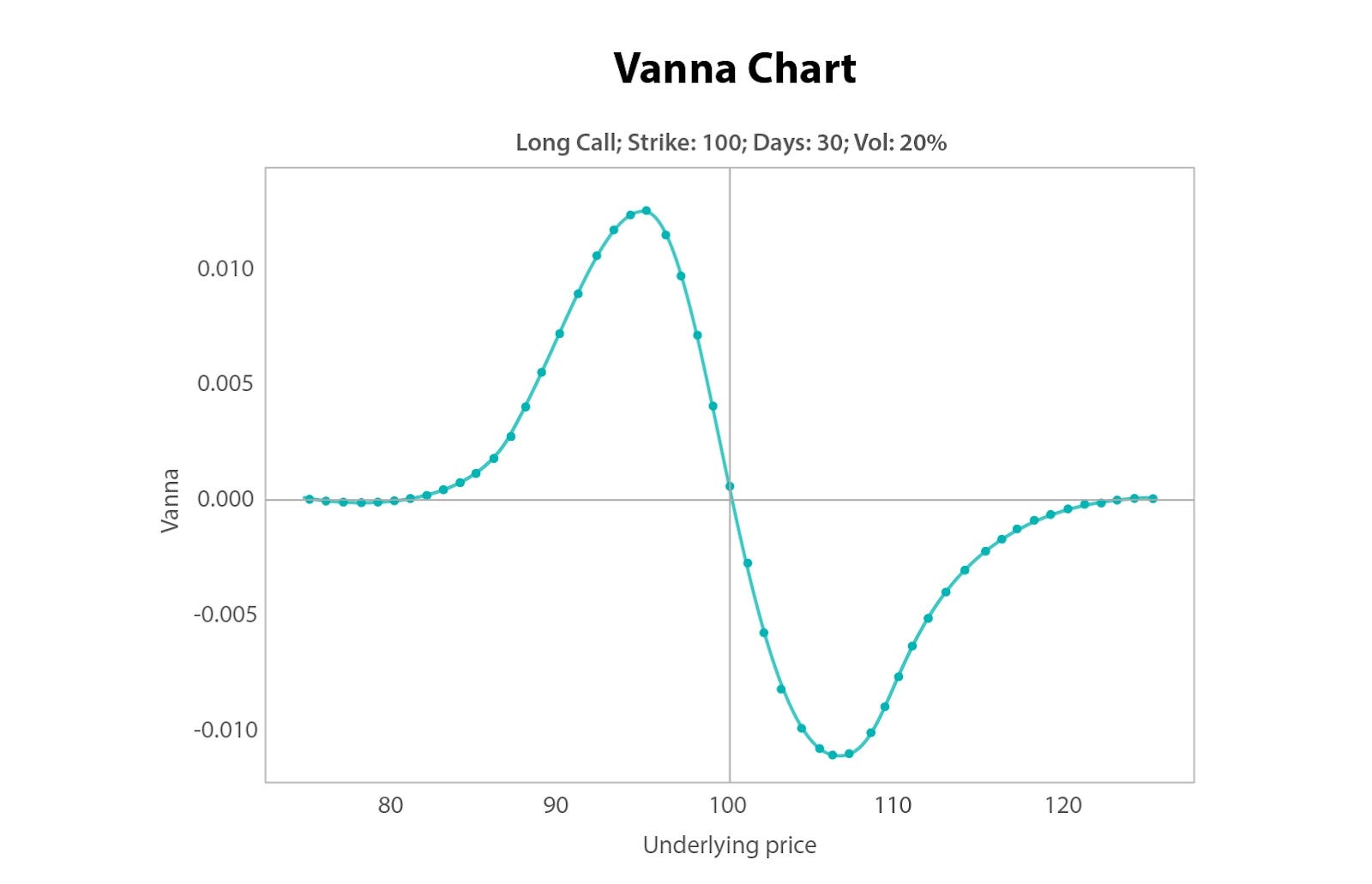

The Interaction Between Vega and Gamma

This is where things get spicy. Gamma measures how fast Delta changes. Vega measures volatility sensitivity. They interact in ways that surprise most traders.

Near expiration, options have very little Vega but very high Gamma. A 0-day-to-expiry option barely moves from volatility changes, but it accelerates violently as the stock approaches the strike. Long-dated options have high Vega and low Gamma. The opposite.

Why does this matter for your long calls and long puts? Because if you're holding a long-dated position, Vega is your primary Greek after Delta. You need to care about it more than Gamma. If you're holding a short-dated position, Gamma dominates, and Vega is almost irrelevant.

Mistake I see constantly: traders buy 30-day options (moderate Vega) and treat them like 7-day options. They ignore volatility entirely. Then IV shifts and they're confused. Don't be that trader.

---

Common Questions About How Vega Affects Long Calls and Long Puts

Does Vega affect long calls and long puts equally?

No. Both are positively exposed to Vega, meaning they gain when implied volatility rises and lose when it falls. However, the magnitude can differ due to skew. Puts often trade at higher implied volatilities than calls, especially during market stress. So a long put might have a higher Vega than an equivalent long call at the same strike and expiration.

Can a long call lose money even if the stock goes up because of Vega?

Absolutely. This is called 'IV crush.' If you buy a long call when implied volatility is inflated (e.g., before earnings), a drop in IV can offset the gains from the stock moving in your favor. It's one of the most common ways retail traders get burned.

What's the best way to avoid Vega losses on long options?

Enter trades when implied volatility is low or average. Use defined risk strategies like vertical spreads to reduce your Vega exposure. And always check the IV percentile before clicking submit. If IV is historically high, wait for a pullback in vol before going long.

Should I buy long calls or long puts during a high VIX environment?

It depends on your thesis. High VIX means options are expensive. If you buy long calls or long puts when VIX is elevated, you're fighting Vega from the start. You need a very large directional move to overcome the cost of the premium. Typically, buying options during low vol and selling them during high vol is the more consistent approach.

How do I calculate Vega for my position?

Your broker's option chain or trading platform shows Vega per contract. It's expressed as the dollar change per 1% change in implied volatility. For example, if Vega is 0.05 and IV drops 2%, your option loses $0.10 per share ($10 per contract). It's that simple.